MULTI ASSET DIVERSIFIED X INDEX

The BNP Paribas Multi Asset Diversified X Index (“the Index”) is a rules-based index that aims to provide exposure to a range of asset classes and geographic regions based on momentum investing principles. The Index is comprised of nine components – four equity futures indices, three bond futures indices and two commodity futures indices.

Daily, the Index selects the combination of components (“the Portfolio”) with the highest past performance for a defined level of volatility and weighting constraints. The Index also aims to keep short-term annualized volatility at 5% and implements a layer of trend risk control when recent returns have been negative by allocating a portion of its weight to a non-remunerable cash exposure.

For more information on the Index performance and statistics, please click here. For a list of selected risks and considerations with the Index, please click here.

THE MULTI ASSET DIVERSIFIED X INDEX INCLUDES

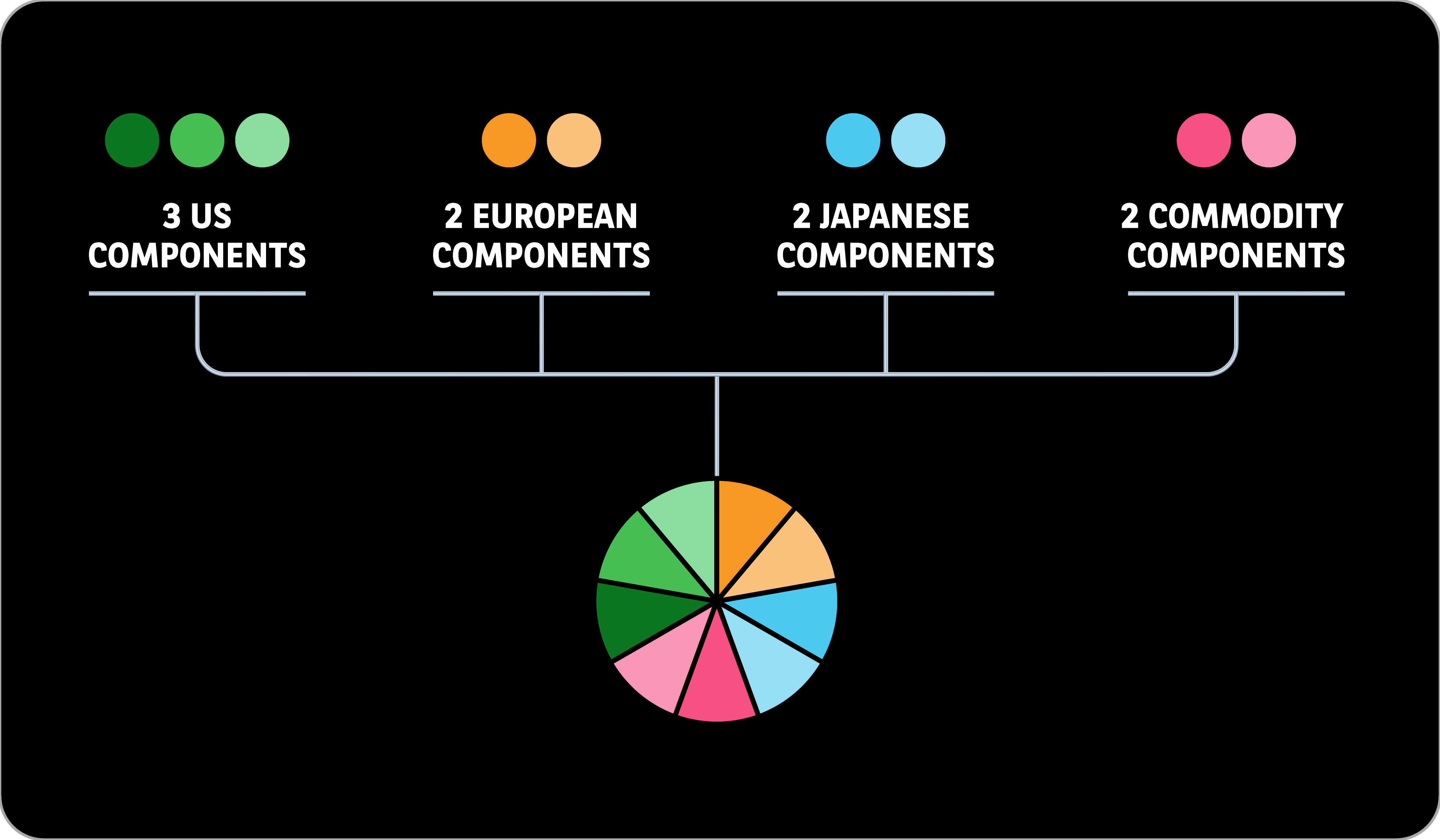

STEP 1

BROAD DIVERSIFICATION

The Index is comprised of 9 components, covering 3 asset classes (equities, bonds and commodities) and 3 regions (US, Europe and Japan).

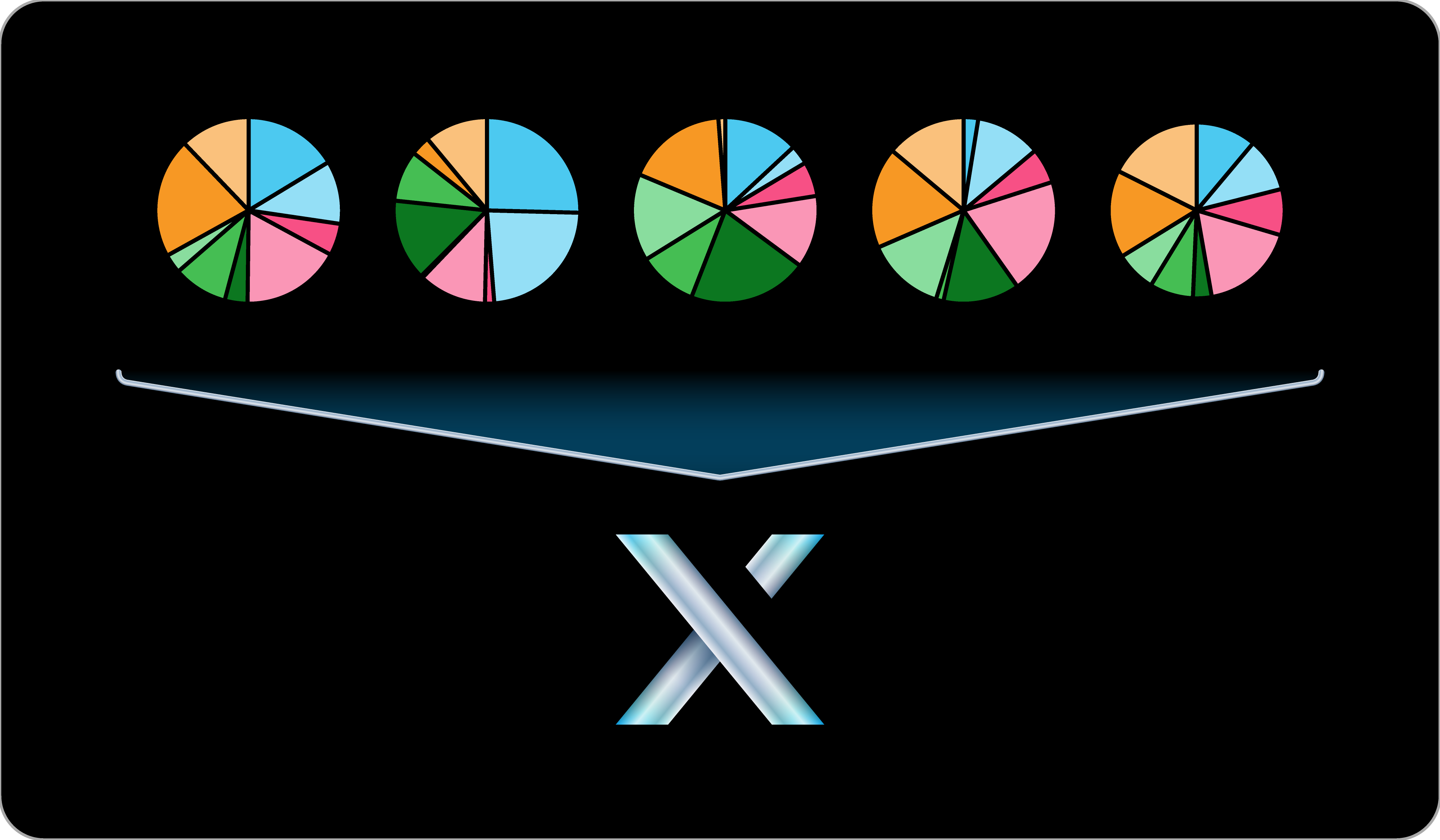

STEP 2

DYNAMIC ALLOCATION

Daily, the Index identifies eligible portfolios, different combinations of the 9 components with respect to defined weighting constraints*. The Index then selects the eligible Portfolio with the highest past performance (based on its trend over the last 1-year) for a defined level of volatility.

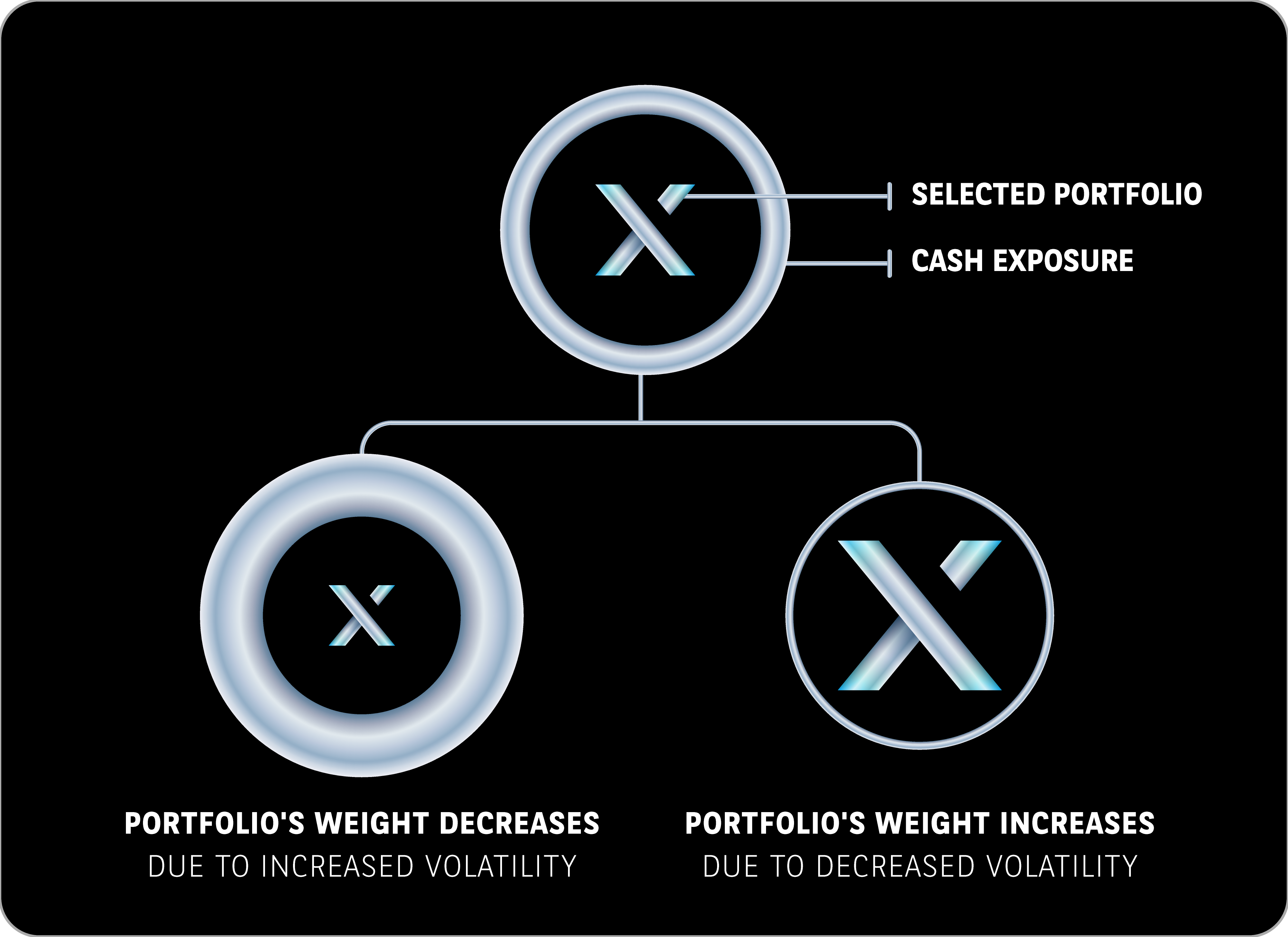

STEP 3

DAILY VOLATILITY CONTROL

The Index targets a short-term annualized volatility of 5%. When short-term volatility of the Portfolio is above 5%, the Index will decrease the Portfolio’s weight and increase the weight of the non-remunerable cash exposure, and vice-versa.

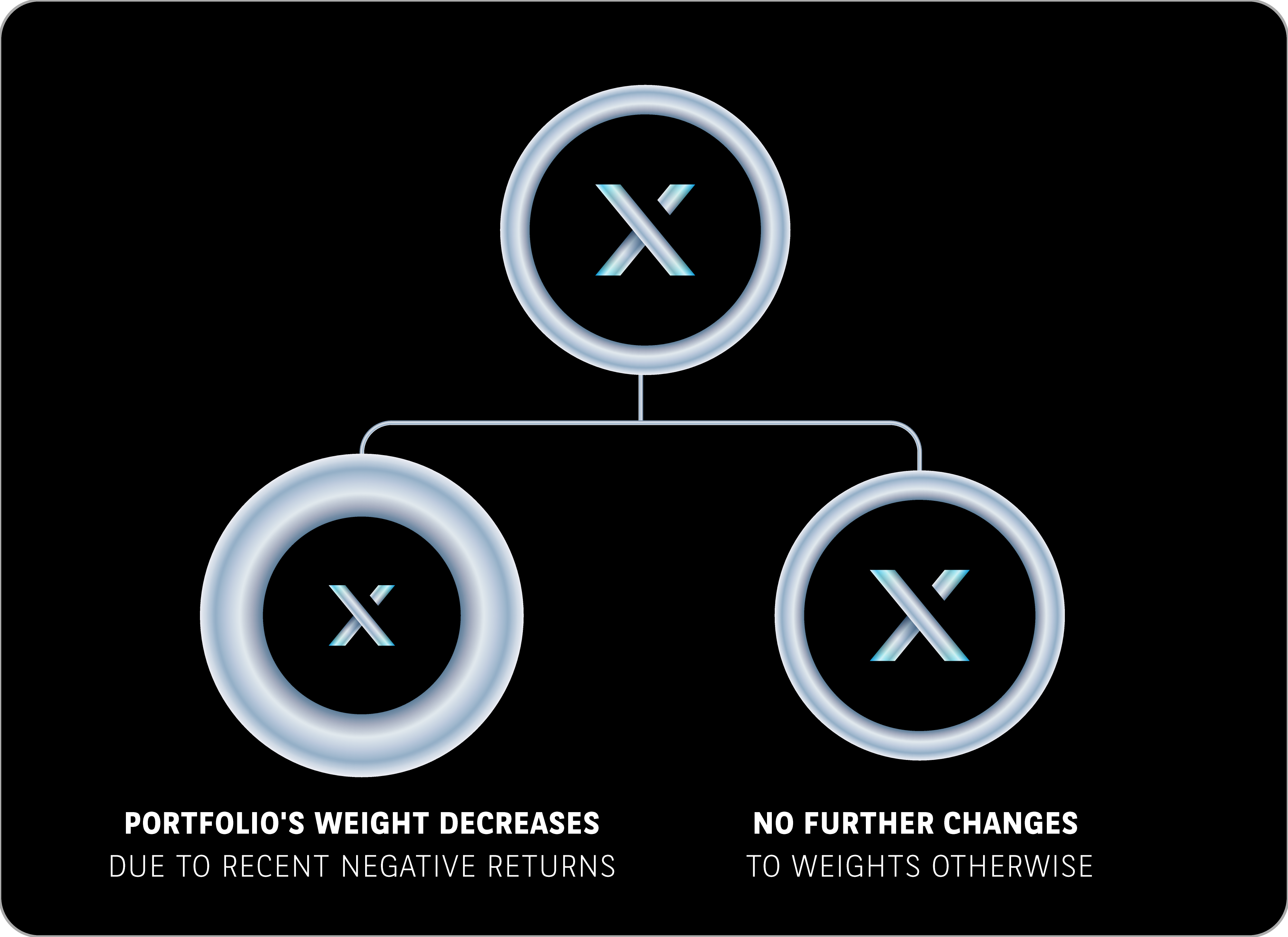

STEP 4

DAILY TREND RISK CONTROL

As the final step, if the trend in the Portfolio’s returns over the last 150 business days has been negative, the Index will decrease the Portfolio’s weight (up to 25%) and increase the weight of the non-remunerable cash exposure.

*Components’ maximum weights: 25% per equity futures index, 25% per bond futures index, and 25% per commodity futures index. 5% is the minimum weight for each US equity futures index, 0% is the minimum weight for each other component, and the sum of all components’ weights is capped at 200% (i.e., leverage is allowed). Daily, the absolute change in the weight of each US equity futures index and bond futures index is capped at 10%, and the absolute change in the weight of each other component is capped at 5%. The cost of borrowing on any non-remunerable cash exposure is zero.

BNP Paribas Multi Asset Diversified X, the global index that brings together diversified returns

with volatility management and adapts to overall market trends.